Statsmodels

Contents

Statsmodels#

Setup#

%matplotlib inline

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

import statsmodels.formula.api as smf

from statsmodels.tools.eval_measures import mse, rmse

sns.set_theme(style="ticks", color_codes=True)

Data preparation#

# See notebook "Data Exploration" for details about data preprocessing

from case_duke_data_prep import *

Data splitting#

train_dataset = df.sample(frac=0.8, random_state=0)

test_dataset = df.drop(train_dataset.index)

Modeling#

Train the model#

# Fit Model

lm = smf.ols(formula='price ~ area', data=train_dataset).fit()

# Short summary

lm.summary().tables[1]

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 8.593e+04 | 6.21e+04 | 1.383 | 0.171 | -3.78e+04 | 2.1e+05 |

| area | 167.7007 | 20.741 | 8.085 | 0.000 | 126.391 | 209.010 |

# Full summary

lm.summary()

| Dep. Variable: | price | R-squared: | 0.462 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.455 |

| Method: | Least Squares | F-statistic: | 65.37 |

| Date: | Wed, 05 Jan 2022 | Prob (F-statistic): | 7.56e-12 |

| Time: | 22:37:38 | Log-Likelihood: | -1053.3 |

| No. Observations: | 78 | AIC: | 2111. |

| Df Residuals: | 76 | BIC: | 2115. |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 8.593e+04 | 6.21e+04 | 1.383 | 0.171 | -3.78e+04 | 2.1e+05 |

| area | 167.7007 | 20.741 | 8.085 | 0.000 | 126.391 | 209.010 |

| Omnibus: | 26.589 | Durbin-Watson: | 2.159 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 107.927 |

| Skew: | -0.862 | Prob(JB): | 3.66e-24 |

| Kurtosis: | 8.499 | Cond. No. | 9.16e+03 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 9.16e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

To obtain single statistics:

# Adjusted R squared

lm.rsquared_adj

0.4553434818683253

# R squared

lm.rsquared

0.4624169431427626

# AIC

lm.aic

2110.625966301898

train_dataset.info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 78 entries, 26 to 73

Data columns (total 7 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 price 78 non-null int64

1 bed 78 non-null int64

2 bath 78 non-null float64

3 area 78 non-null int64

4 year_built 78 non-null int64

5 cooling 78 non-null category

6 lot 78 non-null float64

dtypes: category(1), float64(2), int64(4)

memory usage: 4.5 KB

# Add the regression predictions (as "pred") to our DataFrame

train_dataset['y_pred'] = lm.predict()

# MSE

mse(train_dataset['price'], train_dataset['y_pred'])

31402336646.61913

# RMSE

rmse(train_dataset['price'], train_dataset['y_pred'])

177207.04457390832

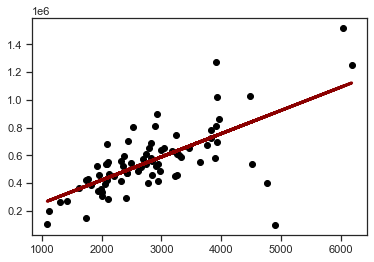

# Plot regression line

plt.scatter(train_dataset['area'], train_dataset['price'], color='black')

plt.plot(train_dataset['area'], train_dataset['y_pred'], color='darkred', linewidth=3);

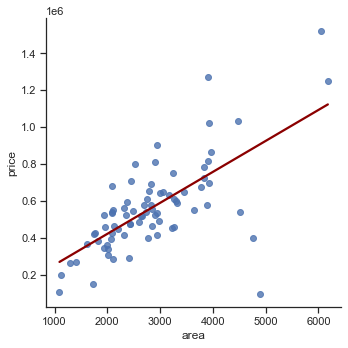

# Plot with Seaborn

import seaborn as sns

sns.set_theme(style="ticks")

sns.lmplot(x='area', y='price', data=train_dataset, line_kws={'color': 'darkred'}, ci=False);

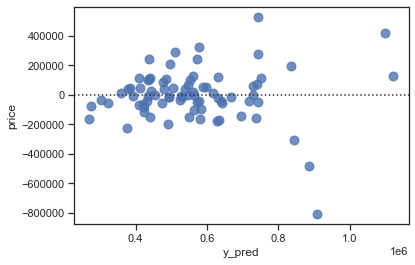

sns.residplot(x="y_pred", y="price", data=train_dataset, scatter_kws={"s": 80});

Validation with test data#

# Add regression predictions for the test set (as "pred_test") to our DataFrame

test_dataset['y_pred'] = lm.predict(test_dataset['area'])

test_dataset.head()

| price | bed | bath | area | year_built | cooling | lot | y_pred | |

|---|---|---|---|---|---|---|---|---|

| 9 | 650000 | 3 | 2.0 | 2173 | 1964 | other | 0.73 | 450348.456333 |

| 12 | 671500 | 3 | 3.0 | 2200 | 1964 | central | 0.51 | 454876.375736 |

| 21 | 645000 | 4 | 4.0 | 2300 | 1969 | central | 0.47 | 471646.447601 |

| 25 | 603000 | 4 | 4.0 | 3487 | 1965 | central | 0.61 | 670707.200633 |

| 36 | 615000 | 3 | 3.0 | 2203 | 1954 | other | 0.63 | 455379.477892 |

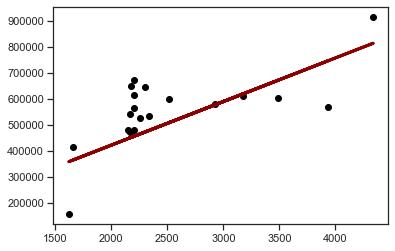

# Plot regression line

plt.scatter(test_dataset['area'], test_dataset['price'], color='black')

plt.plot(test_dataset['area'], test_dataset['y_pred'], color='darkred', linewidth=3);

sns.residplot(x="y_pred", y="price", data=test_dataset, scatter_kws={"s": 80});

# RMSE

rmse(test_dataset['price'], test_dataset['y_pred'])

119345.88525637302

Multiple regression#

lm_m = smf.ols(formula='price ~ area + bed + bath + year_built + cooling + lot', data=train_dataset).fit()

lm_m.summary()

| Dep. Variable: | price | R-squared: | 0.626 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.595 |

| Method: | Least Squares | F-statistic: | 19.83 |

| Date: | Wed, 05 Jan 2022 | Prob (F-statistic): | 1.86e-13 |

| Time: | 22:37:42 | Log-Likelihood: | -1039.1 |

| No. Observations: | 78 | AIC: | 2092. |

| Df Residuals: | 71 | BIC: | 2109. |

| Df Model: | 6 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -2.944e+06 | 2.26e+06 | -1.302 | 0.197 | -7.45e+06 | 1.56e+06 |

| cooling[T.other] | -1.021e+05 | 3.67e+04 | -2.778 | 0.007 | -1.75e+05 | -2.88e+04 |

| area | 111.8295 | 25.915 | 4.315 | 0.000 | 60.156 | 163.503 |

| bed | 5121.5208 | 3.1e+04 | 0.165 | 0.869 | -5.68e+04 | 6.7e+04 |

| bath | 2.678e+04 | 2.94e+04 | 0.910 | 0.366 | -3.19e+04 | 8.55e+04 |

| year_built | 1491.1176 | 1157.430 | 1.288 | 0.202 | -816.732 | 3798.968 |

| lot | 3.491e+05 | 8.53e+04 | 4.094 | 0.000 | 1.79e+05 | 5.19e+05 |

| Omnibus: | 27.108 | Durbin-Watson: | 1.919 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 112.999 |

| Skew: | -0.874 | Prob(JB): | 2.90e-25 |

| Kurtosis: | 8.632 | Cond. No. | 4.57e+05 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 4.57e+05. This might indicate that there are

strong multicollinearity or other numerical problems.