XGBoost

Contents

XGBoost#

XGBoost (eXtreme Gradient Boosting) is a machine learning library which implements supervised machine learning models under the Gradient Boosting framework.

In this tutorial we’ll cover how to perform XGBoost regression in Python. We will focus on the following topics:

How to define hyperparameters

Model fitting and evaluating

Obtain feature importance

Perform cross-validation

Hyperparameter tuning

Setup#

%matplotlib inline

import warnings

warnings.simplefilter(action='ignore', category=FutureWarning)

import numpy as np

import pandas as pd

from pandas import MultiIndex, Int64Index

import matplotlib.pyplot as plt

import xgboost as xgb

print("XGB Version:", xgb.__version__)

from sklearn import datasets

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_squared_error

from sklearn.inspection import permutation_importance

from sklearn.model_selection import GridSearchCV

XGB Version: 1.5.0

Data#

We use data drawn from the 1990 U.S. Census to predict median house value for households within a block (see this data description for more information).

Data import#

X, y = datasets.fetch_california_housing(return_X_y=True, as_frame=True)

feature_names = X.columns

X.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 20640 entries, 0 to 20639

Data columns (total 8 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 MedInc 20640 non-null float64

1 HouseAge 20640 non-null float64

2 AveRooms 20640 non-null float64

3 AveBedrms 20640 non-null float64

4 Population 20640 non-null float64

5 AveOccup 20640 non-null float64

6 Latitude 20640 non-null float64

7 Longitude 20640 non-null float64

dtypes: float64(8)

memory usage: 1.3 MB

Data splitting#

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.1, random_state=0)

Model building#

Hyperparameters#

XGBoost provides many hyperparameters but we will only consider a few of them (see the XGBoost documentation for an complete overview).

Note that we will use the scikit-learn wrapper interface:

objective: determines the loss function to be used likereg:squarederrorfor regression problems,binary:logisticfor logistic regression for binary classification ormulti:softmaxto do multiclass classification using the softmax objectiv (note that there are more options).n_estimators: Number of gradient boosted trees. Equivalent to number of boosting rounds.max_depth: Maximum tree depth for base learners.learning_rate: Boosting learning rate (xgb’s “eta”). Range is [0,1].subsample: Subsample ratio of the training instance. Setting it to 0.5 means that XGBoost would randomly sample half of the training data prior to growing trees.colsample_bytree: Subsample ratio of columns when constructing each tree. Subsampling occurs once for every tree constructed.colsample_bylevel: Subsample ratio of columns for each level. Subsampling occurs once for every new depth level reached in a tree. Columns are subsampled from the set of columns chosen for the current tree.gamma: Minimum loss reduction required to make a further partition on a leaf node of the tree. A higher value leads to fewer splits.reg_alpha: L1 regularization term on weights (xgb’s alpha). A large value leads to more regularization.reg_lambda: L2 regularization term on weights (xgb’s lambda).eval_metric(default is according to objective). Evaluation metrics for validation data, a default metric will be assigned according to objective (rmsefor regression, andloglossfor classificationestimator ).random_state: Random number seed.early_stopping_rounds: If you have a validation set, you can use early stopping to find the optimal number of boosting rounds. Early stopping requires at least one set in evals. If there’s more than one, it will use the last. Note that we include this parameter in our fit function.

Define hyperparameters as dictionary:

params = {

"objective": "reg:squarederror",

"n_estimators":100,

"max_depth": 4,

"learning_rate": 0.01,

"subsample": 0.8,

"colsample_bytree": 0.9,

"colsample_bylevel": 0.8,

"reg_lambda": 0.1,

"eval_metric": "rmse",

"random_state": 42,

}

Fit model#

reg = xgb.XGBRegressor(**params)

Since we want to plot the learning curves for both training and test data, we need to provide both training and test data as eval_set. Furthermore, if you provide a validation set, you can use “early stopping” to find the optimal number of boosting rounds (early stopping requires at least one set in evals. If there’s more than one, it will use the last).

Note

Early stoping: The model will train until the validation score stops improving. Validation error needs to decrease at least every early_stopping_rounds to continue training.

If early stopping occurs, the model will have two additional fields:

reg.best_score,reg.best_iteration

Note

Xgboost will always return a model from the last iteration, not the best one.

reg.fit(X_train,

y_train,

verbose=False,

eval_set= [(X_train, y_train), (X_test, y_test)],

early_stopping_rounds= 3

)

XGBRegressor(base_score=0.5, booster='gbtree', colsample_bylevel=0.8,

colsample_bynode=1, colsample_bytree=0.9, enable_categorical=False,

eval_metric='rmse', gamma=0, gpu_id=-1, importance_type=None,

interaction_constraints='', learning_rate=0.01, max_delta_step=0,

max_depth=4, min_child_weight=1, missing=nan,

monotone_constraints='()', n_estimators=100, n_jobs=10,

num_parallel_tree=1, predictor='auto', random_state=42,

reg_alpha=0, reg_lambda=0.1, scale_pos_weight=1, subsample=0.8,

tree_method='exact', validate_parameters=1, verbosity=None)

Save model#

Save the model into JSON format:

reg.save_model("regressor.json")

Evaluation#

Obtain all evaluation results:

results = reg.evals_result()

Coefficient of determination#

Return the coefficient of determination (\(R^2\)) of the prediction:

# for training data

reg.score(X_train, y_train, sample_weight=None)

0.30197816458883875

# for test data

reg.score(X_test, y_test, sample_weight=None)

0.30315081477332295

RMSE#

XGBoost functions#

Show evaluation result (

rmse) for our test data (validation_1) for the last model in the list (-1)

results['validation_1']['rmse'][-1]

0.978616

Next, we obtain our best iteration (this attribute is 0-based, for instance if the best iteration is the 100th round, then best_iteration is 99).

best_iter = reg.best_iteration

best_iter

99

Show result for best iteration (in our case, the last iteration and best iteration are identical)

results['validation_1']['rmse'][best_iter]

0.978616

Scikit-learn functions#

Next, we use the scikit-learn workflow to obtain our evaluation metrics.

Make predictions

y_pred = reg.predict(X_test)

Obtain RMSE with skicit-learn function

mean_squared_error:

mean_squared_error(y_test, y_pred, squared = False)

0.9786155477422379

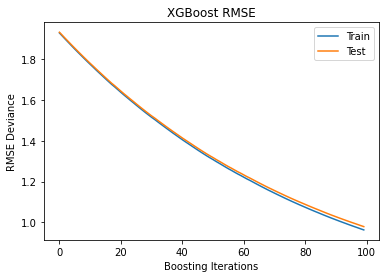

Train test deviance#

Plot training test deviance

# Prepare x-axis

epochs = len(results['validation_0']['rmse'])

x_axis = range(0, epochs)

fig, ax = plt.subplots()

ax.plot(x_axis, results['validation_0']['rmse'], label='Train')

ax.plot(x_axis, results['validation_1']['rmse'], label='Test')

plt.title('XGBoost RMSE')

plt.xlabel("Boosting Iterations")

plt.ylabel("RMSE Deviance")

plt.legend(loc="upper right");

Visualize tree#

You need to install graphviz to plot the tree (for Anaconda, use conda install python-graphviz)

plt.rcParams['figure.figsize'] = [50, 10]

xgb.plot_tree(reg ,num_trees=0);

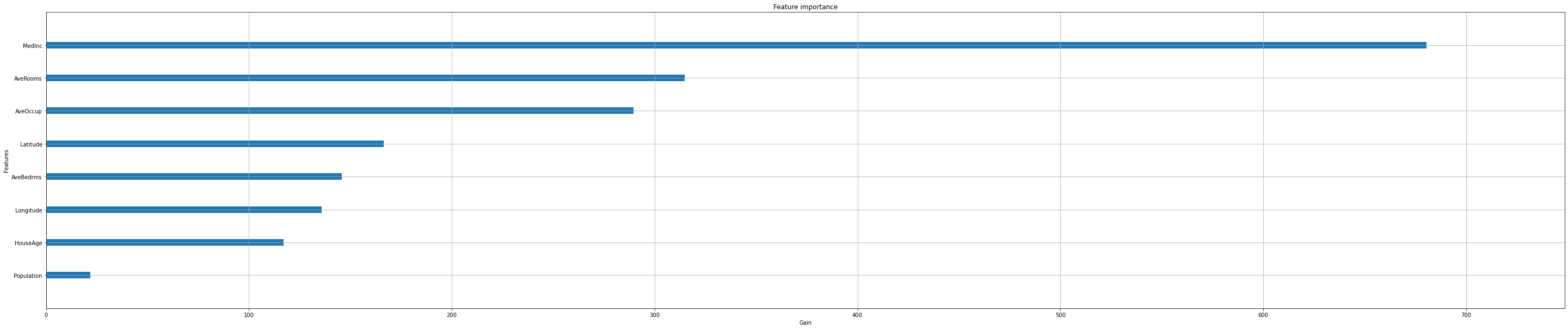

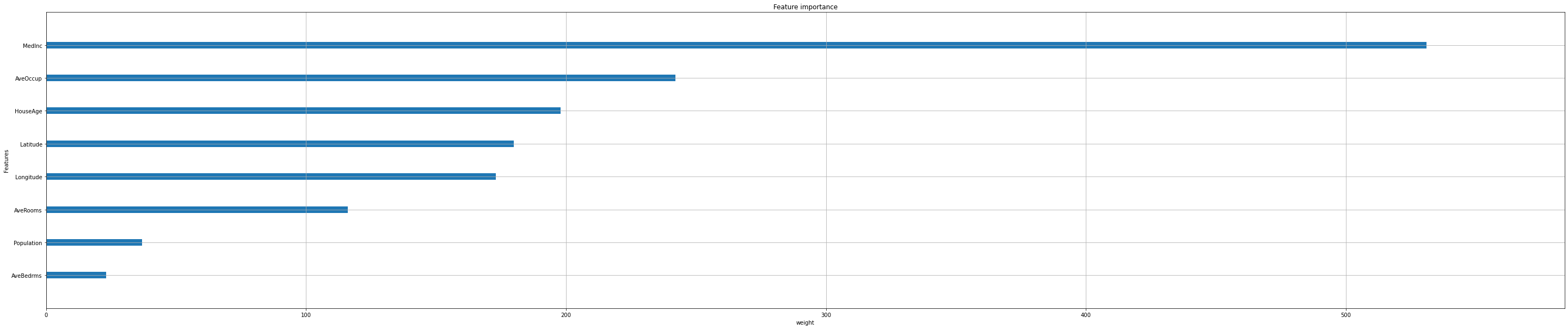

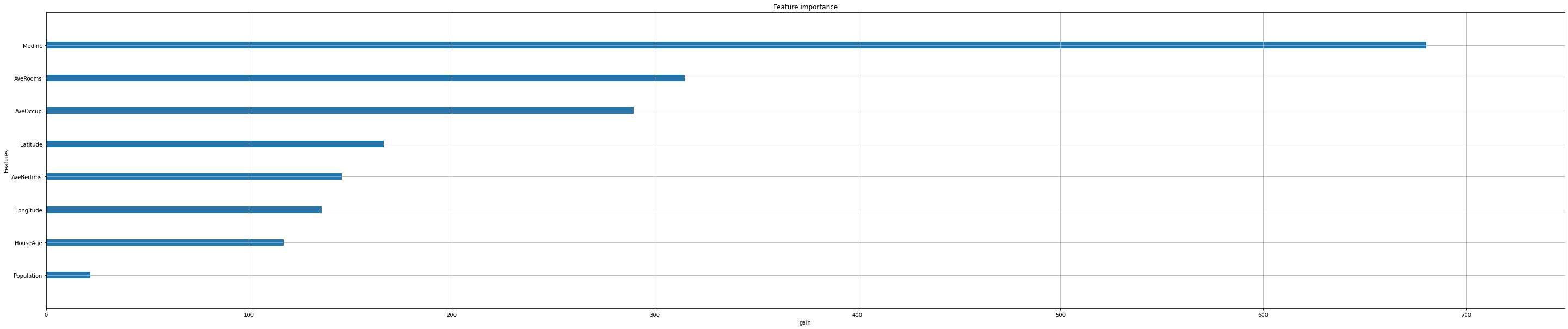

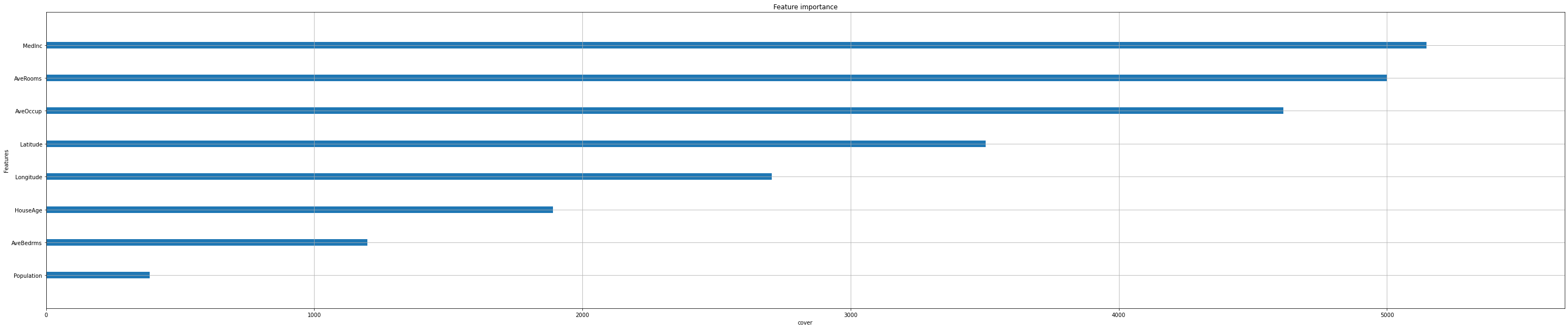

Feature importance#

Next, we take a look at the tree based feature importance and the permutation feature importance.

Feature importance#

Importance is calculated with either “weight”, “gain”, or “cover”

”weight” is the number of times a feature appears in a tree

”gain” is the average gain of splits which use the feature

”cover” is the average coverage of splits which use the feature (where coverage is defined as the number of samples affected by the split)

reg.feature_importances_

array([0.36361885, 0.06250317, 0.16818316, 0.07790712, 0.01166479,

0.15469895, 0.08890022, 0.07252376], dtype=float32)

Feature importances are provided by the function

plot_importance

xgb.plot_importance(reg,

importance_type="gain",

show_values=False,

xlabel="Gain");

Iterate over all options:

feat_importance = ["weight", "gain", "cover"]

for i in feat_importance:

xgb.plot_importance(reg,

importance_type=i,

show_values=False,

xlabel=i);

Permutation feature importance#

The permutation feature importance is defined to be the decrease in a model score when a single feature value is randomly shuffled.

Note

Visit this notebook to learn more about permutation feature importance.

We will use the scikit-learn function

permutation_importance:

result = permutation_importance(

reg, X_test, y_test, n_repeats=10, random_state=42

)

# make a pandas data series

tree_importances = pd.Series(result.importances_mean, index=feature_names)

# sort features according to importance

sorted_idx = np.argsort(tree_importances)

pos = np.arange(sorted_idx.shape[0])

# plot feature importances

plt.barh(pos, tree_importances[sorted_idx], align="center")

plt.yticks(pos, np.array(feature_names)[sorted_idx])

plt.title("Feature Importance (MDI)")

plt.xlabel("Mean decrease in impurity");

Same data plotted as boxplot:

plt.boxplot(

result.importances[sorted_idx].T,

vert=False,

labels=np.array(feature_names)[sorted_idx],

)

plt.title("Permutation Importance (test set)")

plt.show()

Cross-validation#

Next, we use k-fold cross validation to build even more robust trees.

First, we will convert the dataset into an optimized data structure called Dmatrix.

dmatrix = xgb.DMatrix(data=X,label=y)

We use the same hyperparameteras as before.

We just drop

num_estimatorsand instead usenum_boost_roundin our fit.

params_cv = {

"objective": "reg:squarederror",

"max_depth": 4,

"learning_rate": 0.01,

"subsample": 0.8,

"colsample_bytree": 0.9,

"colsample_bylevel": 0.8,

"reg_lambda": 0.1,

"eval_metric": "rmse",

"random_state": 42,

}

Perform 3-fold-cross-validation:

reg_cv = xgb.cv(dtrain=dmatrix,

nfold=3,

params=params_cv,

num_boost_round=5,

early_stopping_rounds=10,

metrics="rmse",

as_pandas=True,

seed=123)

reg_cv.head()

| train-rmse-mean | train-rmse-std | test-rmse-mean | test-rmse-std | |

|---|---|---|---|---|

| 0 | 1.930837 | 0.008074 | 1.930872 | 0.016105 |

| 1 | 1.914908 | 0.008166 | 1.914989 | 0.015754 |

| 2 | 1.898777 | 0.008120 | 1.898905 | 0.015530 |

| 3 | 1.882705 | 0.008067 | 1.882887 | 0.015337 |

| 4 | 1.866842 | 0.007958 | 1.867077 | 0.015233 |

Extract and print the final boosting round metric.

print((reg_cv["test-rmse-mean"]).tail(1))

4 1.867077

Name: test-rmse-mean, dtype: float64

Hyperparameter Tuning#

Let’s demonstrate hyperparameter tuning for some parameters:

params = { 'max_depth': [3,6],

'learning_rate': [0.01, 0.05],

'n_estimators': [3, 5],

'colsample_bytree': [0.3, 0.7]}

reg_h = xgb.XGBRegressor(seed = 42)

reg_hyper = GridSearchCV(estimator=reg_h,

param_grid=params,

scoring='neg_mean_squared_error',

verbose=1)

reg_hyper.fit(X_train, y_train)

Fitting 5 folds for each of 16 candidates, totalling 80 fits

GridSearchCV(estimator=XGBRegressor(base_score=None, booster=None,

colsample_bylevel=None,

colsample_bynode=None,

colsample_bytree=None,

enable_categorical=False, gamma=None,

gpu_id=None, importance_type=None,

interaction_constraints=None,

learning_rate=None, max_delta_step=None,

max_depth=None, min_child_weight=None,

missing=nan, monotone_constraints=None,

n_esti...bs=None,

num_parallel_tree=None, predictor=None,

random_state=None, reg_alpha=None,

reg_lambda=None, scale_pos_weight=None,

seed=42, subsample=None, tree_method=None,

validate_parameters=None, verbosity=None),

param_grid={'colsample_bytree': [0.3, 0.7],

'learning_rate': [0.01, 0.05], 'max_depth': [3, 6],

'n_estimators': [3, 5]},

scoring='neg_mean_squared_error', verbose=1)

print("Best parameters:", reg_hyper.best_params_)

print("Lowest RMSE: ", np.sqrt(-reg_hyper.best_score_))

Best parameters: {'colsample_bytree': 0.7, 'learning_rate': 0.05, 'max_depth': 6, 'n_estimators': 5}

Lowest RMSE: 1.57744988482794